- Home

- >

- Market Rumours

- >

- 4 REASONS THE RALLY MAY MELT DOWN

4 REASONS THE RALLY MAY MELT DOWN

Rating:

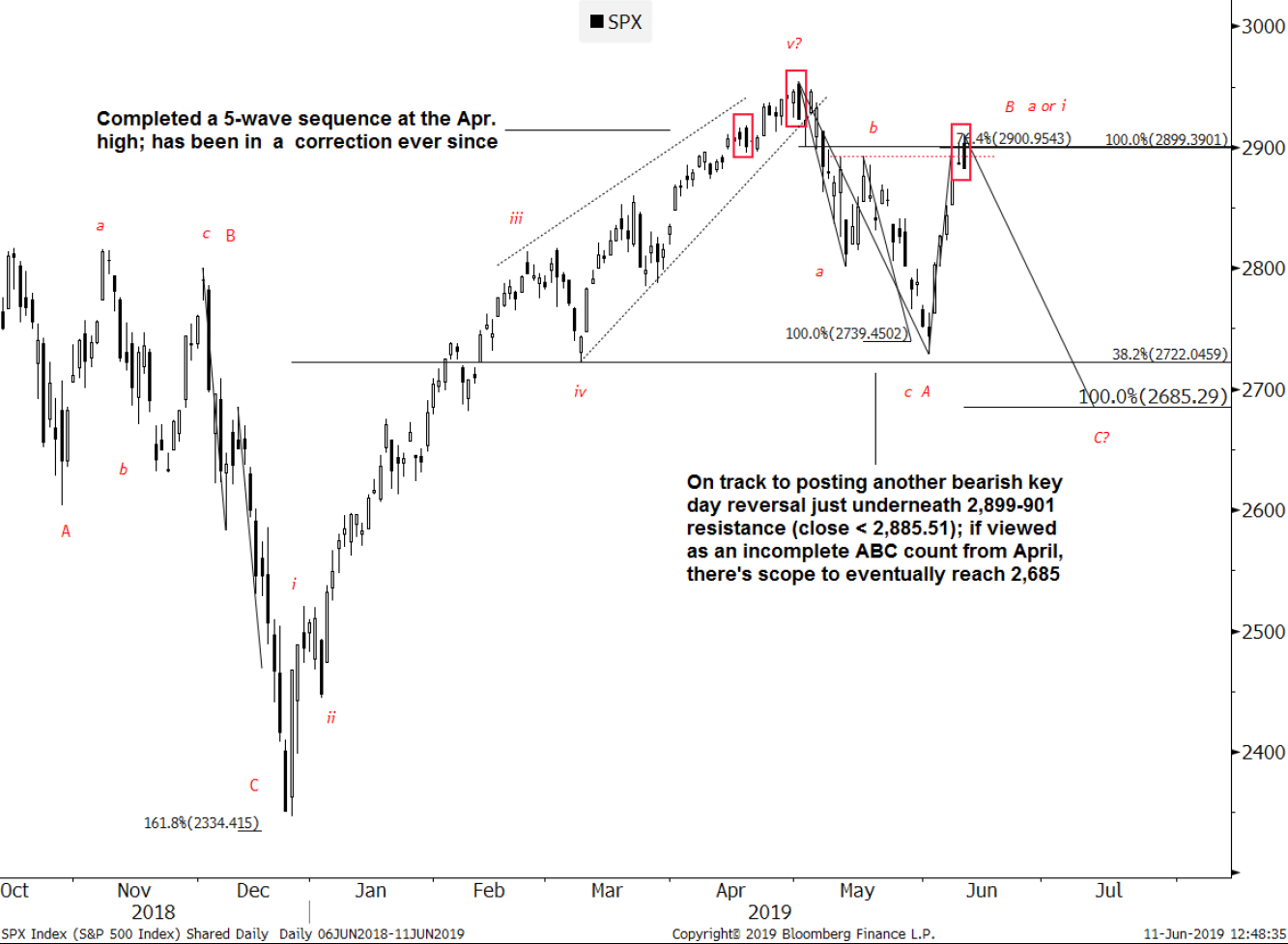

The S&P 500’s June rally has brought the index back within 2% of its all-time highs, stirring memories of a similarly euphoric rise in early 2018. Last week saw more than 20% of S&P 500 companies reach 52-week highs, the most since January 2018 when the index marked the best month it had seen in two years, according to Bloomberg. But amid all the bullish optimism, several market watchers are waving warning flags as they point to a number of reasons why this year might be different and the current melt-up could quickly turn into a meltdown.

4 REASONS THE RALLY MAY MELT DOWN

Defensive stocks leading the market's rise

Fed dovishness feeding a complacent herd mentality

Volatility “fear gauge” on the rise

Forecasts of weaker earnings growth in 2020

What It Means for Investors

Jeff deGraaf, co-founder of Renaissance Macro Research, is one skeptic of the current market euphoria, explaining that the recent stock rebound is being led by defensive sectors. While tech and cyclicals led the market’s rise in 2018, deGraaf says this time it’s utilities, real estate, and consumer staples that are doing all the heavy lifting, having risen by at least 15% over the past 12 months. That’s about triple the rise in the S&P 500. The preference for defensive stocks suggests investors are not as confident as the current rally might lead some to believe.

While Federal Reserve Chairman Jerome Powell’s dovish comments last week may have helped to boost that confidence, they also serve to feed the complacency of the herd currently propping up the bull market, according to Charles Hugh Smith, author of the Two Minds blog. The Fed may have calmed markets and given investors new hope, but by doing so it may be fuelling the conditions for the next crash.

“Confidence in the absolute efficacy of Fed intervention breeds complacency, which is the essential backdrop of stock market crashes,” wrote Smith. “Crashes don’t arise from a skittish herd, they arise from a complacent herd.”

Smith outlined the anatomy of a crash, illustrating how crashes are often preceded by a whipsawing of the market with bears short-selling on deteriorating fundamentals and bulls then rushing in to buy the dip. Eventually, the recurrent bounces fail to reach previous highs, reflecting the waning of investor confidence and precipitating the crash. Even the Fed’s presumed omnipotence suffers a loss of confidence with reassuring messages and even interest rate cuts failing to stop the hemorrhaging.

Another indicator suggesting investor confidence is becoming shaky is the recent rise in the CBOE Volatility Index (VIX), also known as the market’s fear gauge. Over the past several years the VIX only reached its currently lofty level when equities were weakening and it’s the first time since 2009 that the index has failed to decline amid such steep gains in stocks. Macro Risk Advisor’s derivatives strategist Vinay Viswanathan suggests the positive correlation between stocks and volatility is a sign that despite the rise in stocks, there is still plenty of risk.

Adding to the pessimism, Morgan Stanley recently came out with a downward revision of forecasts for corporate earnings. In its base-case scenario, the bank expects earnings to grow by 0% in 2020, as trade uncertainty and modest increases in trade tensions continue to weigh on business confidence and investment. If the forecast is correct, it will mark the second consecutive year of zero earnings growth since 2015-2016.

While there is still much risk and a potential for fundamentals to continue deteriorating, a lot of the downside is due to ongoing trade conflicts between the U.S. and China. If the two countries can work out a trade deal sooner rather than later, the outlook for economic growth may be enough to revive waning confidence and eliminate much of the risk.

Trader Georgi Bozhidarov

Trader Georgi Bozhidarov Read more:

If you think, we can improve that section,

please comment. Your oppinion is imortant for us.