- Home

- >

- FX Daily Forecasts

- >

- Buy yen in crisis? Not this year

Buy yen in crisis? Not this year

Rating:

The trade is familiar to investors worldwide: in times of turmoil, rush for cover by buying the Japanese yen.

This year a global trade row has erupted, Donald Trump has lamented the dollar's strength - ignoring a custom that U.S. presidents avoid openly interfering in financial markets - and the Chinese yuan has tumbled.

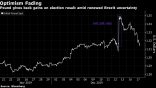

And yet the yen has stayed resolutely weak, becoming the weakest of the G10 developed market currencies this month.

The yen's safe-haven status is not in doubt, underpinned by Japan's nearly two trillion yen ($18 billion) monthly trade surplus. But without a massive world market shock to discourage Japanese investors from buying foreign assets, the yen is likely to stay weak - above all because the Bank of Japan lags behind its central bank peers in ending monetary stimulus.

The Secret Indicators of the Bank Traders

Investors doubt the BOJ can aggressively reduce the stimulus measures as inflation remains well below target and corporate profits are recovering slowly.

The BOJ is debating policy changes to make its stimulus "more sustainable", sources told Reuters, but this pushed the yen up only briefly on Monday.

"The Bank of Japan is still pursuing easing which is still prompting domestic investors to borrow yen and buy overseas assets," said Anton Eser, CIO at Legal and General Investment Management which manages 983 billion pounds ($1.29 trillion) in assets.

While U.S. interest rates have risen seven times since 2016 and the European Central Bank plans to wind down its bond purchases by end-2018, the BOJ is still buying local securities, albeit at a slower pace.

Japanese investors are therefore likely to keep pouring money into foreign assets, despite global market wobbles.

Their net purchases of foreign equities reached 1.5 trillion yen in June, the highest in nearly three years. Even as the trade row deepened, they bought 371 billion yen of overseas stocks during the first week of July.

However, Japanese funds are growing reluctant to hedge exposure to billions of dollars' of U.S. assets.

"I suspect some investors are reducing currency hedge on their foreign bond investments," a senior trader at a major Japanese bank in Tokyo told Reuters, requesting anonymity.

Top rules of the successful trader

Japanese fund managers buying 10-year U.S. Treasuries on a fully hedged basis now earn a slim 33 basis points in yield, compared with 50-80 bps last year. As the Federal Reserve keeps raising interest rates, even that yield advantage could vanish.

And a lack of demand for yen from investors in the currency forwards market would feed into falling spot market demand.

"Currency hedging costs have risen rapidly. Japanese investors have stopped hedging. That stops them buying the yen. The flow is for selling yen," said Adam Cole, chief currency strategist at RBC in London.

Another source of yen selling is Japanese companies making acquisitions overseas due to lackluster economic growth and a shrinking population at home. Thomson Reuters data shows Japanese investors spent a record 13.0 trillion yen on foreign acquisitions in the first half of the year.

These included Takeda Pharmaceutical's (T:4502) $62 billion acquisition of London-listed drugmaker Shire Plc (L:SHP).

Initially the deal helped to push the British pound up more than four percent against the yen in early-April, but in May traders started to buy dollars on news that Takeda's payment to Shire shareholders would be in dollars.

Trade conflict would seem yen-positive by raising global market volatility. In fact, this is helping to push it down.

Japan is vulnerable to a trade war. Autos, for instance, comprise almost 30 percent of its exports to the United States and new U.S. tariffs could hurt Tokyo's vaunted trade surplus.

Also, as fund managers worldwide cut foreign investment holdings, much of this cash is going to U.S. markets instead of the "safe havens". The dollar is likely to benefit from a trade war due to the United States' lower reliance on exports.

"Rather than move into the Swiss franc or the Japanese yen, the widening interest rate differential in favor of the U.S. dollar is currently providing investors with a strong alternative," Rabobank currency strategist Jane Foley said.

Global investors now hold their biggest overweight position in U.S. equities in 17 months, Bank of America (NYSE:BAC) Merrill Lynch's poll showed last week. Other equity holdings have fallen and allocations to Japan slid for the third time in four months.

Correlation has been high this year between Japanese stocks and the yen, with both losing ground, BAML's FX strategist Kamal Sharma noted. That's unusual because yen weakness usually boosts the Nikkei average (N225).

"If U.S. share markets crumbled, then we would be in a different situation," the Tokyo-based trader said. "But as long as Wall Street is in the risk-on mode, the dollar will be supported against the yen."

Source: Reuters

Chart: Used with permission of Bloomberg Finance L.P.

Trader Aleksandar Kumanov

Trader Aleksandar Kumanov Read more:

NZD/JPY – Short with the main movement after a price action signal

NZD/JPY – Short with the main movement after a price action signal The only expiring FX options today are for GBP/USD and they are in a small size

The only expiring FX options today are for GBP/USD and they are in a small size Jeffrey Gundlach: “USD’s next move is going to be down”

Jeffrey Gundlach: “USD’s next move is going to be down” What’s ahead for the Australian dollar for the next year

What’s ahead for the Australian dollar for the next year B.J.’s new Brexit strategy wasn’t approved by the Pound

B.J.’s new Brexit strategy wasn’t approved by the Pound

If you think, we can improve that section,

please comment. Your oppinion is imortant for us.