- Home

- >

- Daily Accents

- >

- Focus from the markets in 2019? The balance sheet of the FED

Focus from the markets in 2019? The balance sheet of the FED

Rating:

Interest rates were fashionable in 2018. Now, when it comes to the Federal Reserve policy of 2019, markets signal that they will start concentrating on any potential changes in their portfolio.

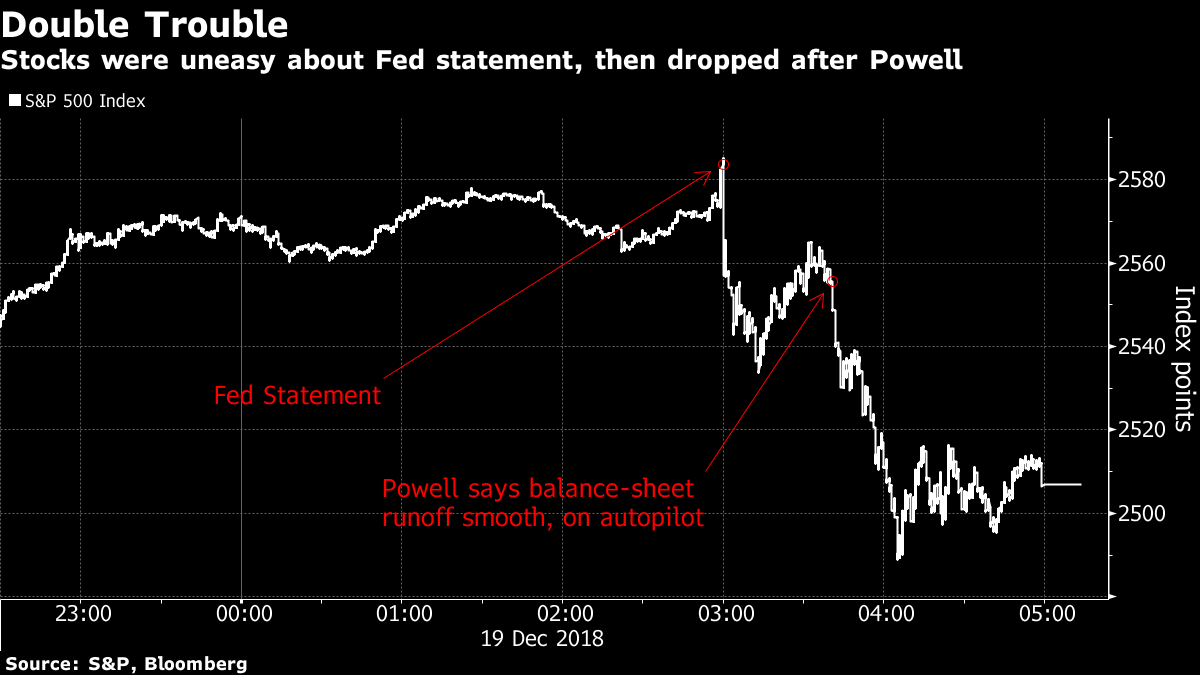

The Fed on Wednesday made a forecast for just two interest rates in the next year, instead of three and above all - far from the initial forecast for four. JPMorgan Chase, Deutsche Bank and Goldman Sachs also cut their long-term expectations of monetary policy. None of this, however, satisfied investors' expectations, especially following Jerome Powell's comments, that quantification will continue at the current pace.

Right at this point, the shares turned sharply down, and the government securities started rallying. Confirming the FED's position to stick to its current move has been seen as quite aggressive by the markets, strongly denying gradual withdrawal of incentives.

Yield on 30-year bonds dropped by a few more points to 2.97% yesterday after the previous day at the FED meeting yield fell by 9 points. Powell failed to present the pre-Christmas gift everyone was expecting.

FED economists have long considered quantitative facilities as a mechanical process rather than as an active policy tool. Adapting the FED's balance sheet to monetary policy sounds pretty simple and at the same time "compelling" instead of directly denying the benefit of this adaptation as just an instrument. 18 months ago, Janet Yellen determined the effect of policy weakening as ... "looking at the wall as it dries".

But Powell on Wednesday said at a press conference that the process really progressed smoothly on "autopilot". Investor disappointment was the only logical thing to follow. The S & P500 fell by 1.5%. 10-year bonds fell to 2.75%, the lowest since April. There is a clear division between renewed investor hypersensitivity to changes in the Fed's balance sheet and its direct effects on financial conditions and markets, of course. The main disappointment came from the clear signal that the pace with which it had to reduce the balance was not in the FED's plans for discussion, at least for now. It is the market reaction in equities and bonds that signals the desire to speed up this process and normalize the situation.

Futures coupled with the key interest rate suggest that traders even no longer appreciate even a raise in the interest rate for 2019. If this turns out to be the scenario and the markets remain turbulent, Powell and his colleagues will just make another " point "of their dot plan or, in other words, will further mitigate their intentions of further tightening.

What could be more effective at one point is the opportunity to "release" the Fed's portfolio at $ 50 billion a month.

Discussion on the balance will be a hot topic again in 2019. With just half a rating for one interest rate pick-up next year, there is no longer a significant buffer for the Central Bank to feel comfortable pulling out of the plan if prospects become - dark.

Some see signs of market implications this year, namely from QE transit to QT. Although no economy had experienced a recession in 2018, most of the assets owned by Deutsche Bank reported a negative return that occurred for the first time in a century.

First, the Federals must become a little bit clearer to the markets and society about their intentions to balance and what their state should be. Secondly, we have to accept the fact that we are going through a period of quantitative tightening, how hard it will be and how long will be the issues that will long disturb the investors.

Source: Bloomberg Finance L.P.

Graphs: Used with permission of Bloomberg Finance L.P.

Trader Martin Nikolov

Trader Martin Nikolov Read more:

Risk off after the escalation in the Middle East, markets are recovering in a period of calm

Risk off after the escalation in the Middle East, markets are recovering in a period of calm The macroeconomic events for today’s trading calendar

The macroeconomic events for today’s trading calendar The US government has confirmed the attacks, Trump is calling an emergency staff meeting

The US government has confirmed the attacks, Trump is calling an emergency staff meeting Has the war between Iran and the US started?

Has the war between Iran and the US started? US markets remain under pressure, traders await Iran’s response

US markets remain under pressure, traders await Iran’s response

If you think, we can improve that section,

please comment. Your oppinion is imortant for us.