- Home

- >

- Market Rumours

- >

- Low interest rates in the US as a trap for developing economies

Low interest rates in the US as a trap for developing economies

Rating:

With the high rates growing level of debt in developing economies. From 2009 to 2014 of USD obligations of non-US economic units increased more than double from $ 2 trillion to $ 4.5 trillion. This expense included foreign US companies and banks, and also disposed of by foreign companies bonds in USD. In the period before the crisis, companies from developing countries have a share of around 30% in total external indebtedness dollar. Today, this share exceeds 50%. Only in China, $ 200 billion in 2008, USD-day obligations exceed $ 1 trillion. Borrowers in dollars are guided by very simple logic, when placed on the financial markets bonds USDte will pay many times lower cost of this debt than the interest rates in their own countries. Here it comes as a huge (often state-owned) companies primarily BRICS, and small companies, Lodha Group Indian or South African Eskom. The management of the borrowers in this simple way to increase profits data calculated from the local base interest rates. On the other side are the investors who receive a higher dollar returns against the US issued similar instruments. Thus the interests of borrowers and lenders match laboriously at this for quite a reasonable period. This trend is growing and naturally cause a number of negatives, including a sharp change in the exchange rates of local currencies and increasingly visible shortage of USD. Local central banks are forced to make more dollar volume interventions, but the result is rather unsatisfactory.

The central banks of industrialized countries face a different problem. First they first of its existence encounter the phenomenon negative interest rates, which implies a lack of historical data and models for reaction. Another problem created stereotype that you have to control two basic indicators (unemployment and inflation) that correlate with each other absolutely opposite. Today, unemployment reached quite acceptable levels and Evrozaonata in the US, but the inflation virtually absent. The measures taken by repurchases in the US and UK did not lead to serious results, stopping them and the idea that rising employment will boost inflation also not obtained so far. It remains possible third negative scenario - collapse, bankruptcies and possible banking crisis in developing countries.

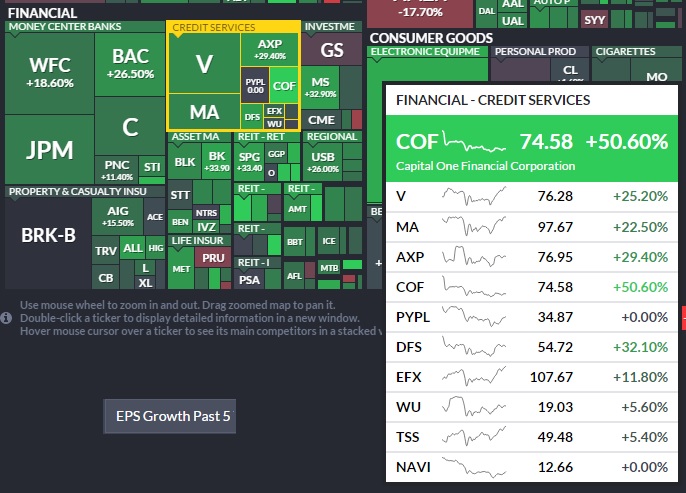

Against this background it is interesting US-Financial sector, which for the past five years recorded one of the largest rate in EPS-growth (past 5 years), particularly pronounced at Credit Services.

Varchev Traders

Varchev Traders If you think, we can improve that section,

please comment. Your oppinion is imortant for us.