- Home

- >

- Fundamental Analysis

- >

- The mess with the REPO market and what it is

The mess with the REPO market and what it is

Rating:

When a system works perfectly, you don't need to think about it. This is usually also the case with a vital but disguised part of the financial system, also known as the REPO market, where huge amounts of money and assets are exchanged every day. However, when there is a problem with this mechanism, as it happened in mid-September, attention is again turned to the Federal Reserve. The Fed has taken steps to calm the nervous markets by pumping billions of dollars, but is that enough?

What is the REPO market?

The place where heaps of money the sea of assets meet. An appointment that is valued at $ 3 trillion of debt that is refinanced daily. REPO is short for repurchase agreements - transactions that equate to short-term loans, often occurring in the evening. REPO deals allow large investors - such as mutual funds - to make money by giving short-term loans (cash) that would otherwise be set aside. This enables banks, brokers and dealers to get the financing they need, and in return they give away their assets. The healthy REPO market helps a huge number of transactions run smoothly - including the hassle-free $ 16 trillion bond market.

How is the Fed involved in all this?

In several ways. For years, central banks around the world have used their own REPO market to temporarily support lending activity in lower liquid markets, stabilize financial costs and set interest rates. In 2008, the REPO market wiped out and many things have changed completely since then. Since then, the Fed, along with other regulators, have worked hard to control risk and strengthen liquidity as insurance. In 2013, the Fed was a major player in the REPO market, maintaining an interest rate ceiling slightly below the base rate.

What happened?

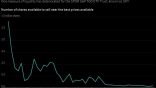

In mid-September, a huge amount of cash leaked out of the market while too many assets were flowing at the same time, resulting in the sudden lack of cash for those in need. This discrepancy caused the night's REPO interest rates to jump to 10% on September 17 and the previous week's level was 2%. More alarming for the FED was that the volatility in the REPO market raised its base interest rate to 2.30%, above the 2.25% upper limit that the Fed had set. Just then, the Fed was preparing to reduce that ceiling to 2%.

Why did all this happen?

According to some analyzes, several different events were a catalyst that occurred at the same moment, in the same direction. A large amount of sovereign debt was poured into the market taken by brokers, just at the moment when the money stopped, at the moment when the institutions had to pay taxes to the state. Others blame post-crisis regulations that slow the banks' process of raising more money by jumping directly into the REPO market. However, according to a BIS report, there are more structural problems that affect REPO activity between the four major US banks and the fact that their portfolios of highly liquid assets have greater access to government securities. Analysts also point to the excessive use of hedge funds in this market.

What did the Fed do at this point?

The first direct cash injection into the banking sector since the financial crisis has poured nearly $ 75 billion over four days. This money was "temporary" to help balance banks' financing and reduce interest rates. This is known as the night-time REPO system, with the Fed giving money to major dealers against government securities or other assets.

Was that enough?

The move calmed markets, with interest rates falling to 2% on September 19. The following week, FED NY began offering temporary loans for more than a day, known as term operations. This forms a more rigorous schedule for REPO operations. Since then, night operations have intensified, offering abundant financing. In October, the Fed began buying $ 60 billion in government securities to restore reserves. However, this heightens investor concerns that a further collapse may occur at the end of the year when banks and all financial institutions end the financial year. To prevent collapse on December 31 this year, the Fed intends to inject nearly half a trillion dollars of liquidity.

What's wrong with analysts?

Some believe that market safety regulations force dealers to withdraw from the market, reducing overall liquidity. This is thought to continue as government spending and national debt continue to rise. The overall perception is that the financial sector is losing out of its reserves, which is a sign that the banking system's buffer zone is cracking during stress.

What does this mean?

This would mean that bank reserves of more than $ 1 trillion would not be enough to cover the need for money in the system. The Fed is buying $ 60 billion of government securities a month, which will continue to H2 by 2020. Powell has repeatedly said that this is not another quantitative easing to support the economy. He stated that in this way they would be better able to control the REPO market.

And what does all this mean?

As with all corporations, the Fed's assets and liabilities must be balanced. In addition to reserves, the bank forms assets from currency circulation, which is growing with the pace of the economy. To prevent this growth from stifling reserve growth, the Fed will need to continue to buy government securities.

What else can the Fed do?

They made one move at their meeting in September and other measures are being discussed. The FOMC reduced the base rate it pays on the so-called. excess reserves - cash that banks leave in the Fed above the limit they have as an interest rate to quell money market stress. Reducing their IOER gives banks the ability to lend more of their money, which keeps the REPO market under control, and the effective Fed interest rates within their range.

What else could the Fed do?

Many market players want the Fed to activate a new tool called standing overnight repo facility. This tool will determine the specific amount to be given to the REPO market every day. According to James Bullard, activating this tool will prevent extreme volatility in money market volatility and keep interest rates in the range.

Source: Bloomberg Finance L.P.

Trader Martin Nikolov

Trader Martin Nikolov Read more:

If you think, we can improve that section,

please comment. Your oppinion is imortant for us.