- Home

- >

- Fundamental Analysis

- >

- This market would only appeal to Gordon Gekko

This market would only appeal to Gordon Gekko

Rating:

Judging by the performance of the markets this week, we can only conclude about the amazing rally with only one conclusion: investors have become too greedy. S & P500 yesterday closed with a new historic peak. Similar is the case for both junk and junction bonds in the emerging markets. Greed, however, we can best see it on the government bond market, which is usually considered to be the "mature" market.

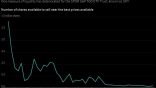

Within a few days, the topics of talks on market participants in bonds have moved from whether the Fed will cut interest rates this year to how much it will reduce them next month. The chances of cutting down by 25 basis points are 100% and the probability of cut by 50 points is 35%. That's why yield on 10-year bonds fell below 2% for the first time since 2016. That there will be cut will be, but it will have to be confirmed by the subsequent economic data. Fed will have to seriously argue for a reduction of 50 basis points, but will they be enough to avoid the negative effects on the economy? Economically, this makes sense to ensure, but are the conditions fundamentally so bad? US GDP growth outlook for this year is 2.8%, 1.2% for the Eurozone and 0.7% for Japan. Also, the financial conditions are already loosened enough, and there are currently no indications that current interest rates restrict business or consumers.

The story shows that betting on the bond market is bound to be foolish. Even so, it does not mean that this market is not subject to corrections or that it is overstated from time to time.

It seems the stock market has forgotten about risk premiums. The S & P500 rises every day this week, raising yields on an annual basis to 17.8%. The main motive for the outburst of this rally is the prospect of lower interest rates, as well as the potential de-stressing tension between the US and China. But investors forget that low interest rates will not help much. Especially for the profits of companies, and there the forecasts are getting worse. Although a year earlier we saw an expansion of the US economy by 3.1%, corporate earnings remained almost flat. The current forecast is that profits will decline for the first quarter by 2.5% from 2018. It is important to note, however, that the companies themselves are realistically reducing their expectations. And now stocks are not so cheap. The market is finding it harder to record new tops against less positive data. However, less positive data would make the Fed withdraw from its cut decision, which is currently the main driver for the markets.

Credit markets are no exception. The price of hedging against US corporate debt with CDW has fallen to its lowest level since September 2018. Like in the stock market, traders have forgotten that the reason a bank is cutting interest rates is due to worsening conditions. The rally in credit markets is also 50/50 with the rising uncertainty surrounding the companies, their creditworthiness and the value of their balance sheets. This is exactly what the International Monetary Fund warns of. They have discovered a crack in corporate debt. Lending to companies with a small credit rating rises and can cause serious damage. UBS predicts that investors could lose about $ 480 billion from junk debt leverage and leverage credits when the credit cycle is over. The US investment debt is now $ 5 trillion. Half of the composite bonds are rated BBB +, BBB or BBB-. These bonds can indeed be a junk rating and follow the domino effect.

Gold appreciates significantly, rising by more than 2.50% yesterday, the largest leap since August 2016. At $ 1389 and already more than $ 1400, gold has not been so expensive since 2013. Given the reputation of gold as a asset - a refuge in tough times, that should be a sign that investors really worry about the economic outlook, right? Maybe not. First, many raw materials, including gold, are traded in US dollars. So when greenbuck gets weaker, it makes raw materials more expensive to buy. And the US currency has definitely begun to experience difficulties. Fed's Cut and Donald Trump signals, which hint at a weak dollar, are now overweight. The appetite for gold also increases. The fact is that global bonds for more than $ 12 trillion with a yield below zero. Many investors are looking to move their money, in which case they choose gold as guarantors rather than bonds. Citigroup even predict that gold may reach $ 1500. Central banks around the world also continue to move away from the US dollar, increasing their reserves in gold.

Source: Bloomberg Finance L.P.

Graphs: Used with permission of Bloomberg Finance L.P.

Photo: Flickr

Trader Martin Nikolov

Trader Martin Nikolov Read more:

If you think, we can improve that section,

please comment. Your oppinion is imortant for us.