- Home

- >

- Stocks Daily Forecasts

- >

- Time couldn’t be worse for a techs crash

Time couldn't be worse for a techs crash

Rating:

I would say that I can think of worse events for a fragile market at a critical time than an antitrust bids for some of the most important companies in America, but that will not be entirely true.

To be clear, this has been obvious for at least 14 months (ie since last March, when privacy concerns and some presidential messages to Amazon shook big tech companies) that antitrust control is probably in the maps for the favorite "big" of the sector. But just because something is well telegraphed does not mean that it will be learned with readiness when the time comes.

In short (and I think the short story is what everyone wants at the moment), the Federal Trade Commission and the Justice Ministry will review possible anti-competitive practices among the big names. This includes Facebook, Amazon and Google. Apparently, Apple will also be examined under the jurisdiction of the Ministry of Justice.

Unfortunately for these companies, the idea that anti-competitive practices are to be sought is shared by some of the most influential politicians on both sides of the path. Elizabeth Warren and President Trump agree on something, and although they may differ as to why just some of the companies listed above must be "looked at" (quoting the president), each of them has called for an increase control. For his part, Trump has repeatedly insisted that Google is biased against conservative media.

I will not go into the details about these samples or judge the corner of the corner - believe it or not, that is one issue in which the policy of the situation does not concern me.

What interests me, however, is the extent to which this news reaches the worst possible moment. Markets are desperately trying to cope with escalation after the escalation of the trading front, and global growth prospects darken the trading sentiment. Major technology companies have been a pillar of market support for years, and these names are so widely held that massive liquidation of stocks may be really bad. Do not forget that the Q4 is characterized by a reversal of the trend for technology companies and that is not well accepted by investors - at all. It is remarkable that on Monday, the Invesco QQQ ETF is less profitable than the SPDR S & P 500 Trust ETF largest margin on June 9, 2017.

Does this date ring a bell? If not - let me elaborate:

June 9, 2017 was the day Goldman published his famous "FANG mispriced" note, which implies, among other things, that crowding out a factor is a risk to the markets.

Goldman's analysis still applies, by the way, but I do not want to go too far for it. On the contrary, I just want to make a few simple observations and then talk a little about the macro.

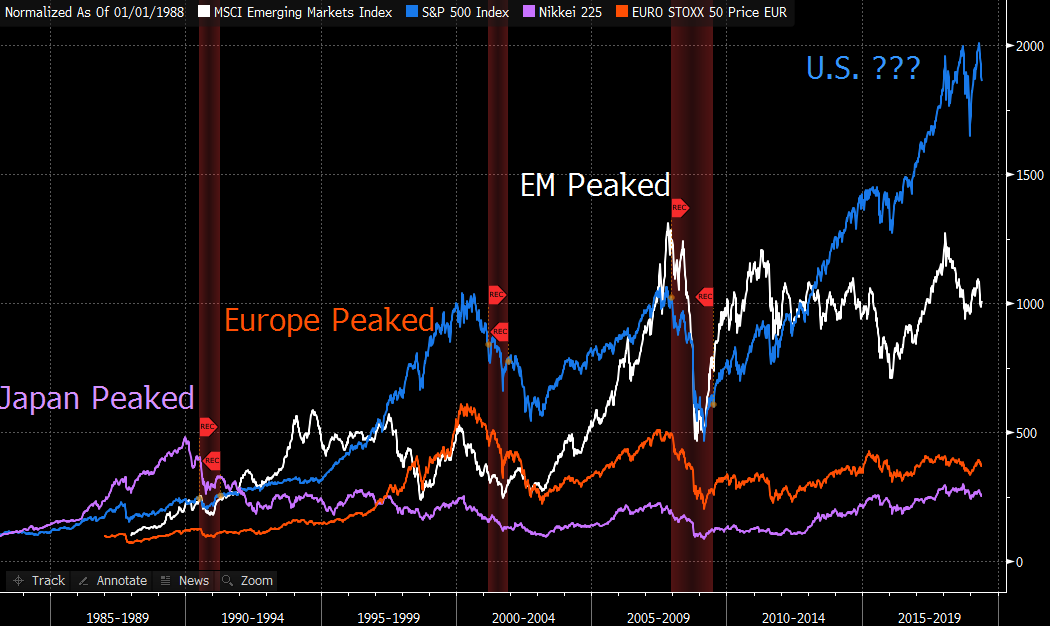

First, these companies are too important to experience some existential crisis on the eve of a possible economic downturn in the United States (and from an "existential crisis," I mean only that everyone is forced to see what the future might look like under different regulatory regimes) .

Even if you accept a benevolent outlet in the war, this cycle is already in its late stages. If you look at the yield curve, we are somewhere in about a year of recession (this is controversial, but I am talking here in general). At the same time, corporate profitability in the US is likely to have reached its highest value, at least for this cycle, and the margin left out of rising labor costs and tariffs are likely to be realized in the future.

The next photo from Goldman's recent presentation (up to May 24th) neatly describes how critical these companies really are (note, for example, the highest growth rates for FAAMG vs. S & P as a whole, and the same margin comparison): growth of FAAMG versus S & P as a whole, and the same margin comparison):

Now, look at the 10 names on Goldman's Hedge Fund VIP Sheet, which quotes the "50 companies whose performance will affect the profits of fund-oriented hedge funds:

Allow me to say once again that attempts to say something on this issue, which is concise and comprehensive at the same time as the deletion of (i) countless questions about how the government can deal with critics' concerns when it comes to for Amazon, Google, and Facebook, and (ii) the potential impact on the market of rethinking these mammoths in Washington is impossible. My point here is just to remind everyone that when it comes to how important these names are on the market, it goes beyond the common sense that because these companies are ubiquitous, they are important.

The latest exciting news (at least from the point of view of everyone who cares only for the short-term direction of the stock) comes on a day when market participants assume the predictable daily dose of ominous titles for a commercial war. On Sunday evening, the New York Times reported that the Trump administration is meditating on Australian strikes last week, and on Monday morning, the Chinese Ministry of Education issued a warning to students and scholars about training in the United States.

Neither of these developments is trivial.

The news in Australia is confusing for obvious reasons (that means we nearly accrued even more tariffs last week in addition to the situation in Mexico and in addition to the Trump administration's decision to abolish the CAP status for India), while China's warning to students confirms analysts' long-standing concerns that the Sino-American dispute is now spreading in areas that have few (if at all) economic and trade-related issues.

At the moment of these news, yield on 10-year government securities fell to 2.07%. That, friends, is unbelievable considering where we were in September and highlights how big the problems of global growth are. Later in the session, ISM Manufacturing posted its lowest values from Trump's management. GAP shares, on the one hand, and ISM, and government bond yields, on the other, is not even close to filling, which, for pessimists among you, suggests that stocks still have somewhere to fall.

Expectations for a fall in the Fed have already been raised in overdrive. On Monday, talks turned around the extent to which Jerome Powell had to cut interest rates this month if he wanted to organize a passive surprise. This is a worrying news because it implies that the Fed simply can not meet market expectations (ie there is no way to be gloomy enough). This, in turn, means that anything less than, say, a 0.25 percent reduction for this month, or an indication that the July meeting is likely to lead to -0.50%. expectations. Nomura's Charlie McElligott said this in a note on Monday morning.

Trader Aleksandar Kumanov

Trader Aleksandar Kumanov Read more:

US – Iran – Iraq tension remain the main driver of the stock market today

US – Iran – Iraq tension remain the main driver of the stock market today How top market players on Wall St think 2020 will look like on financial markets

How top market players on Wall St think 2020 will look like on financial markets Money Flow before the start of the new trading week

Money Flow before the start of the new trading week Cincinnati Financial Corporation (CINF.US) -Opportunity for long positions

Cincinnati Financial Corporation (CINF.US) -Opportunity for long positions Asia stocks gain as Fed signals no rate cuts in 2020

Asia stocks gain as Fed signals no rate cuts in 2020

If you think, we can improve that section,

please comment. Your oppinion is imortant for us.