- Home

- >

- Fundamental Analysis

- >

- What is really behind the rally in risky assets? Let’s follow the money

What is really behind the rally in risky assets? Let's follow the money

Rating:

In explaining why, since the beginning of the year, we have a strong rally and rebound in equities, corporate bonds, and currencies from the EM region, most analysts say: Fed's mood swings. In December, the Central Bank set out the need for several successive rises in interest rates. Last week, President Jerome Powell said the FED could afford patience. But that's only part of a bigger story.

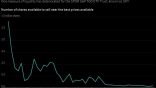

For seven consecutive days, the MSCI All-Country World Index rose, recording its best series in November 2017. Investor and strategist Danielle Lacalle of Tressis SV commented on Twitter how the rally reflects global cash flow recovery. "Forget profits or macro indicators." - writes Lacalle. "This is the reason why markets are recovering." A cash flow index for 12 major economies, including the United States, China, the Eurozone and Japan, shows that their total cash flow peaked at $ 73.11 trillion in April before falling to $ 69.8 trillion in mid-November, then rising again to $ 72.6 trillion in January this year. The common belief is that the increase in cash flows from central banks in order to combat the global financial crisis first is the key cause of the "cosmic" performance of risky assets. This growth is even more pronounced when the index doubled in 2008 to $ 35.3 trillion, just a few months before the global shares take up a rally in which MSCI will double by the beginning of 2018 before the stock issues start again.

The global economy is expected to slow down, and most central banks postpone or slow down their plans to normalize monetary policy by withdrawing some of their excess liquidity, which means "the party" continues. "A modest loosening of global financial conditions is enough to stabilize growth in the second half of 2019" - writes Richard Turnill, chief investment strategist at BlackRock. "Any decisive action in global monetary policy and a change in the fiscal stance towards a more growth-friendly position may launch a renewed bullish market."

AMERICAN STOCKS ARE WEIRD

The US share rally, which led to a 16% rise in the S & P500 index since Christmas, lacks essential elements that usually accompany such a rally. First, the data from the Investment Company Institute show flows to mutual funds in shares that are minimally related to cash outflows in the second half of 2018. Secondly, trading volumes are down significantly, with the S & P500's shares "switching the owner" just a little over the $ 38 billion turnover line across each quarter of the past year. This is a decrease of nearly $ 42 billion in turnover in 2016, and less than half the volume at its peak at the beginning of this century. Third, and perhaps the most unusual, corporate earnings forecasts for this quarter and subsequent periods are rather weak. That is why many strategists predict a "recession" in the reporting season. But among stock investors, hope remains forever. Consensus expectations expect profit growth to slow in the remainder of the year but will rebound rapidly, reflecting an average earnings per share of 9.5% for the period 2019-2020. This is more than the average from 8.2% over the past five years. Also, ratings will soon begin to support the stock. The following price-to-earnings ratio, which compares the S & P500 with its average return over the past 10 years, will begin to rise. BI, however, points out that, soon, the years that are calculated in the pre-crisis ratio will begin to drop out of statistics and calculations, which will give more meaning to stocks, even at moderate levels of corporate growth.

TOO SMALL AND SURELY WITH A BIG DELAY

Economically troubled Italy, which is the Eighth PIIGS acronym during the European debt crisis only a few years ago. Italy is beginning to prepare to sell nearly $ 1.8 billion ($ 2.1 billion) of state property in an attempt to ease the burden of its foolish debt. The Finance Ministry designates property owned by the state and district administrations that could be sold - mostly military polygons and bases, hospitals and office buildings that are no longer in operation. Italy is feeling the tension. According to the data, the state is already in recession for the first time since 2013, with most economists expecting growth to fall even below the government-specified anemic level of 1%. As one of the most indebted countries in the world with a debt of 132% to GDP, such actions are a good signal that the government is trying to get out of the situation. Or at least relieve the burden. But investors have calculated the success of the government. The sale of $ 2 billion in property will lower the tension by only 0.1% of the country's total government debt of $ 2.26 trillion.

AUSTRALIAN UTOPIA CAN END WITH BREAKDOWN

One of the biggest surprises on the world market this year is the Australian dollar. It has risen by more than 2% since the beginning of the year against a basket of nine currencies in developed countries. The Australian's good performance was also on Tuesday when RBA decided not to change interest rates, even after the report, which said that the negative risks have increased both in the world and in Australia. For a currency that remains strong in the face of such an evolution of events is impressive. But it did not come without consequences. The shares of the National Bank "flew" after a long-standing investigation by the Australian government, which triggered actions to restructure the banking scandal and corrupt banking sector. Leaving it aside, it still remains the fact that some economists say that Australia will not be able to avoid its first recession in 28 years. The bubble in the domestic mortgage market is slowly shrinking, and the economy of Australia's main trading partner - China - is cracking.

ECONOMIC RELIEF FOR FARMERS

The trade talks continue with full steam, but they are approaching the deadline of March 1, imposed by Donald Trump. An economic sector relies on high hopes for a positive development of events. Purdue University - CME Group's Monthly Agricultural Economy Barometer posted growth in January at its highest levels since last June. Expectations are calculated on the basis of the opinion of 400 producers and farmers, which shapes their sentiment in terms of the state of health of the country's agricultural sector. They have reached their highest level since February 2017. The good mood among the manufacturers has also spread among investors. Bloomberg Agricultural Subindex rose 5.51% since the beginning of the year. "Our assumption is that the deal will not be concluded in the first quarter but rather in the first half of this year." - notes Juan Lucian, CEO of Archer - Daniels - Midland Co. The good mood comes from the reports that China is again returning to buying soy from the US. US exporters have sold 2.603 million tonnes of soybeans to China for delivery by August 31st.

TEA LEAVES

For those who are optimistic about the good outcome of the US-China talks, it is good to monitor the trade data of both economies. Since Trump began to reduce the trade balance between exports and imports with China, which was one of its goals in the war, trade data on the deficit, import and export levels have become key. If Trump's policy fails to contribute to resolving the conflict, it will lead to more tariffs or an increase in the power of the current. But looking at the trade balance last September, we will see that it is expanding, which means its strategy to break China is not that successful.

Source: Bloomberg Finance L.P.

Graphs: Used with permission of Bloomberg Finance L.P.

Photo: Pixabay

Trader Martin Nikolov

Trader Martin Nikolov Read more:

If you think, we can improve that section,

please comment. Your oppinion is imortant for us.