- Home

- >

- Commodities Daily Forecasts

- >

- Whats next for Iron Ore in four charts

Whats next for Iron Ore in four charts

Rating:

The iron ore market globally is highly volatile by the lasting and widening impact of Vale's deadly breach last month, which shook prices and raised concerns of shortages. After the initial incident in Brazil at the end of January, the largest producer announced a reduction in supplies to 70 million tons, although it is said to try to compensate for some lost production.

As the drama unfolds, investors, consumers and manufacturers are struggling with many unknowns, starting with how much the supply will be losing this year and the next, as executives strive to meet the biggest challenge facing the company. There are other critical variables that will help to influence the price direction that sank on Tuesday for a second day.

After the catastrophe, benchmark spot prices rose to their highest levels in 2017, after which they lost some of their power. Most banks and commentators expect further profits, although the view is divided about how long profits will continue. Citigroup Inc., and the Commonwealth Bank of Australia, marked the outlook for a short-term rise of up to $ 100 per tonne. Fitch Solutions Macro Research increased its $ 60 forecast for the whole year.

The dramatic iron ore rally will increase costs for steelmakers, potentially crossing their profit margins, unless they can shift the extra burden on customers. This will be a critical issue in China, the largest steel producer in the world, accounting for half of world production. Prior to the Vale to deliver a shock of supply, the margins approached the breakeven point in the fourth quarter before rebounding a bit. Higher cost of raw materials will increase pressure on steelmakers and may require further shifting to cheaper ores of lower quality. This is likely to help Australian miners, especially Fortescue Metals Group Ltd.

If Vale's problems limit shipping, can Chinese mills get more ore from China? There is a significant mining industry in the mainland, but production has been hurt in recent years as its content is lower and more expensive than foreign supplies and Chinese producers have been subject to severe environmental restrictions. After the disasters of Vale, Goldman Sachs Group Inc. has raised the prospect of restoring production from non-Brazilian sources, including China. Still, Argonaut Securities Asia Ltd. says local miners will be cautious: "The point is that this is not a cyclical increase, with prices rising from one to two years."

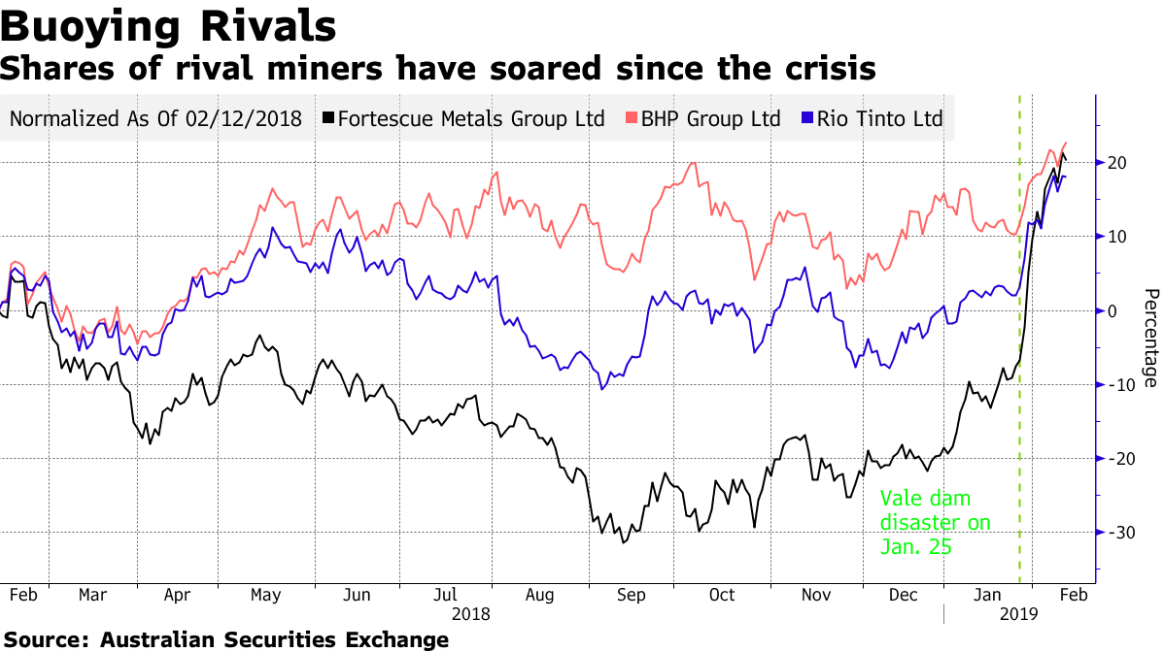

If the mills in China can not get enough extra material from the miners on their doorstep, what's left to other places? Following Vale's tragedy, rival miners - mostly Australia - the most productive nation - have risen, including BHP Group, Rio Tinto Group and Fortescue. Although they will undoubtedly benefit from the higher price, there may be catches when it comes to larger volumes. According to major manufacturers, only Rio will be able to significantly increase supply.

Source: Bloomberg Finance L.P.

Original Post: The Global Iron Ore Crisis: What's Next in Four Charts

Charts: Used with permission from Bloomberg Finance L.P.

Trader Aleksandar Kumanov

Trader Aleksandar Kumanov Read more:

If you think, we can improve that section,

please comment. Your oppinion is imortant for us.